There are many ways to approach financial planning for couples. These strategies can range from consolidating expenses to liquidating an asset. Ultimately, these strategies are aimed at establishing sound financial health for you and your partner. If you are having difficulty choosing the right strategy, it is worth seeking professional guidance. If you are struggling with managing your finances on your own, working with a financial planner is a great solution.

Budgeting for couple's financial planning

Couples must plan their financial future together. This includes the joint expenses, assets and long-term financial goals. It's important to first determine what areas of their budget could be cut. For example, you may need to cut back on housing, groceries, and utilities. You may also want a look at your long-term goals in financial planning, such as saving money for retirement or paying back student loans. It's also important to identify your individual needs, such as hobbies.

If you are worried about a financial emergency in the future, it is important to understand your finances. A monthly breakdown of your spending can provide insight into where you can trim. This can help you decide if it is time to save money for a vacation or pay off your bill. Budgeting is a way to help couples avoid panic. It gives them a plan and allows them save money for the long-term.

Defining and achieving your goals and values

Financial planning includes setting goals and values. Your values can temper or shape the way you spend money. Galinskaya tells the story about a couple who wanted independence for their children but were concerned that they wouldn’t be able pay enough. They discussed their goals and values when they planned for college tuition.

The two of you also need to agree on how much you will spend each goal. S.M.A.R.T. is the best way to accomplish this. S.M.A.R.T. is shorthand for Specific. Measurable. Attainable. Relevant. Time-bound. These goals should be specific, relevant to your lifestyle and relationship, and have specific deadlines. It may seem simple to set a general goal for "saving money", but it's not very specific. Furthermore, it is not measurable and will not be relevant to your relationship.

A rainy day's savings

Even though it can be difficult to save for a rainy-day, there are ways you can make it easier. It's important to establish a budget, and stick to it, in order to stay on the right track. A spreadsheet can be used to determine personal spending limits, and to monitor your finances.

It is impossible to predict when your money will be needed, but it is possible to set aside some. For example, a rainy day fund can cover unexpected expenses like an appliance repair. A rainy day fund is also useful for unexpected expenses such as unexpected medical bills for a child, or pet. It can also help you avoid debt and create new financial opportunities.

Consolidating costs

You can set up joint accounts if you're married and want to consolidate all your expenses. You can share all your assets and track each other's spending by setting up joint accounts. The key to a healthy budget is to establish joint priorities that will guide your financial decisions. Make a budget to show you how much money and where you want it to go each month. You should adjust your budget to reflect changes in income and expenses as you become married. You can also review individual budgets in order to have a full picture of your finances.

Budgeting is easier when you have a joint bank account. For tracking your spending, you can use software that budgets or apps on your smartphone. You can keep track of your finances easily without needing to update spreadsheets or split resources monthly. This account can be used by you to pay expenses for your children if you are a parent.

Financial planners

Although hiring a couple financial advisor can be a good idea, there are some things that you need to know before hiring one. Ask whether the planner is paid commissions for any products he sells. You should also ask how much money the planner makes from selling certain investments, such as annuities and bonds. This will allow you to determine if the planner acts in your best interests.

If you don't want to make financial mistakes, it is worth hiring a professional financial planner. There are dozens of financial experts, each with different titles and responsibilities. Find out their areas of expertise, the fees they charge and whether there are other options.

FAQ

What is wealth management?

Wealth Management is the practice of managing money for individuals, families, and businesses. It covers all aspects related to financial planning including insurance, taxes, estate planning and retirement planning.

What Are Some Examples of Different Investment Types That Can be Used To Build Wealth

There are several different kinds of investments available to build wealth. Here are some examples.

-

Stocks & Bonds

-

Mutual Funds

-

Real Estate

-

Gold

-

Other Assets

Each has its benefits and drawbacks. Stocks and bonds, for example, are simple to understand and manage. However, stocks and bonds can fluctuate in value and require active management. Real estate, on the other hand tends to retain its value better that other assets like gold or mutual funds.

Finding the right investment for you is key. Before you can choose the right type of investment, it is essential to assess your risk tolerance and income needs.

Once you've decided on what type of asset you would like to invest in, you can move forward and talk to a financial planner or wealth manager about choosing the right one for you.

What is estate plan?

Estate Planning refers to the preparation for death through creating an estate plan. This plan includes documents such wills trusts powers of attorney, powers of attorney and health care directives. These documents ensure that you will have control of your assets once you're gone.

What is risk management in investment administration?

Risk management refers to the process of managing risk by evaluating possible losses and taking the appropriate steps to reduce those losses. It involves identifying, measuring, monitoring, and controlling risks.

Risk management is an integral part of any investment strategy. The goal of risk management is to minimize the chance of loss and maximize investment return.

The following are key elements to risk management:

-

Identifying risk sources

-

Monitoring and measuring the risk

-

How to control the risk

-

How to manage risk

How to Beat Inflation by Savings

Inflation refers to the increase in prices for goods and services caused by increases in demand and decreases of supply. It has been a problem since the Industrial Revolution when people started saving money. The government regulates inflation by increasing interest rates, printing new currency (inflation). There are other ways to combat inflation, but you don't have to spend your money.

You can, for example, invest in foreign markets that don't have as much inflation. You can also invest in precious metals. Since their prices rise even when the dollar falls, silver and gold are "real" investments. Investors who are worried about inflation will also benefit from precious metals.

How old should I be to start wealth management

Wealth Management should be started when you are young enough that you can enjoy the fruits of it, but not too young that reality is lost.

You will make more money if you start investing sooner than you think.

If you want to have children, then it might be worth considering starting earlier.

If you wait until later in life, you may find yourself living off savings for the rest of your life.

Statistics

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

- According to Indeed, the average salary for a wealth manager in the United States in 2022 was $79,395.6 (investopedia.com)

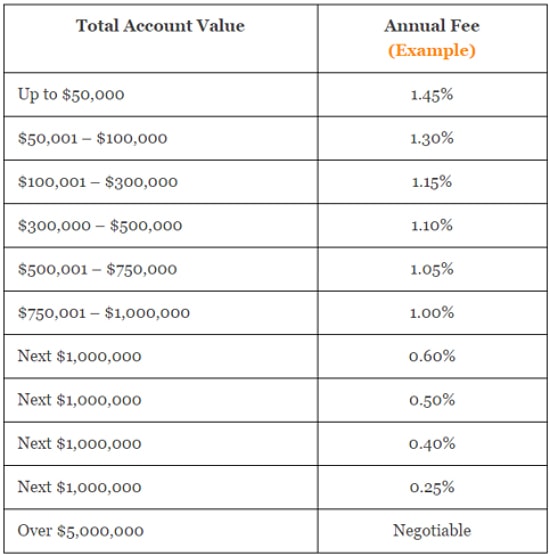

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

External Links

How To

How to become Wealth Advisor

A wealth advisor is a great way to start your own business in the area of financial services and investing. This career has many possibilities and requires many skills. These qualities are necessary to get a job. A wealth advisor's main job is to give advice to investors and help them make informed decisions.

First, choose the right training program to begin your journey as a wealth adviser. It should include courses on personal finance, tax laws, investments, legal aspects and investment management. After completing the course, you will be eligible to apply for a license as a wealth advisor.

These are some helpful tips for becoming a wealth planner:

-

First, learn what a wealth manager does.

-

It is important to be familiar with all laws relating to the securities market.

-

Learn the basics about accounting and taxes.

-

After you complete your education, take practice tests and pass exams.

-

Finally, you need to register at the official website of the state where you live.

-

Apply for a licence to work.

-

Show your business card to clients.

-

Start working!

Wealth advisors typically earn between $40k and $60k per year.

The size and location of the company will affect the salary. The best firms will offer you the highest income based on your abilities and experience.

As a result, wealth advisors have a vital role to play in our economy. Therefore, everyone needs to be aware of their rights and duties. Additionally, everyone should be aware of how to protect yourself from fraud and other illegal activities.